2025 Letter to Stockholders

FROM OUR PRESIDENT, CEO & CIO, PETER FEDERICO

DEAR FELLOW STOCKHOLDERS:

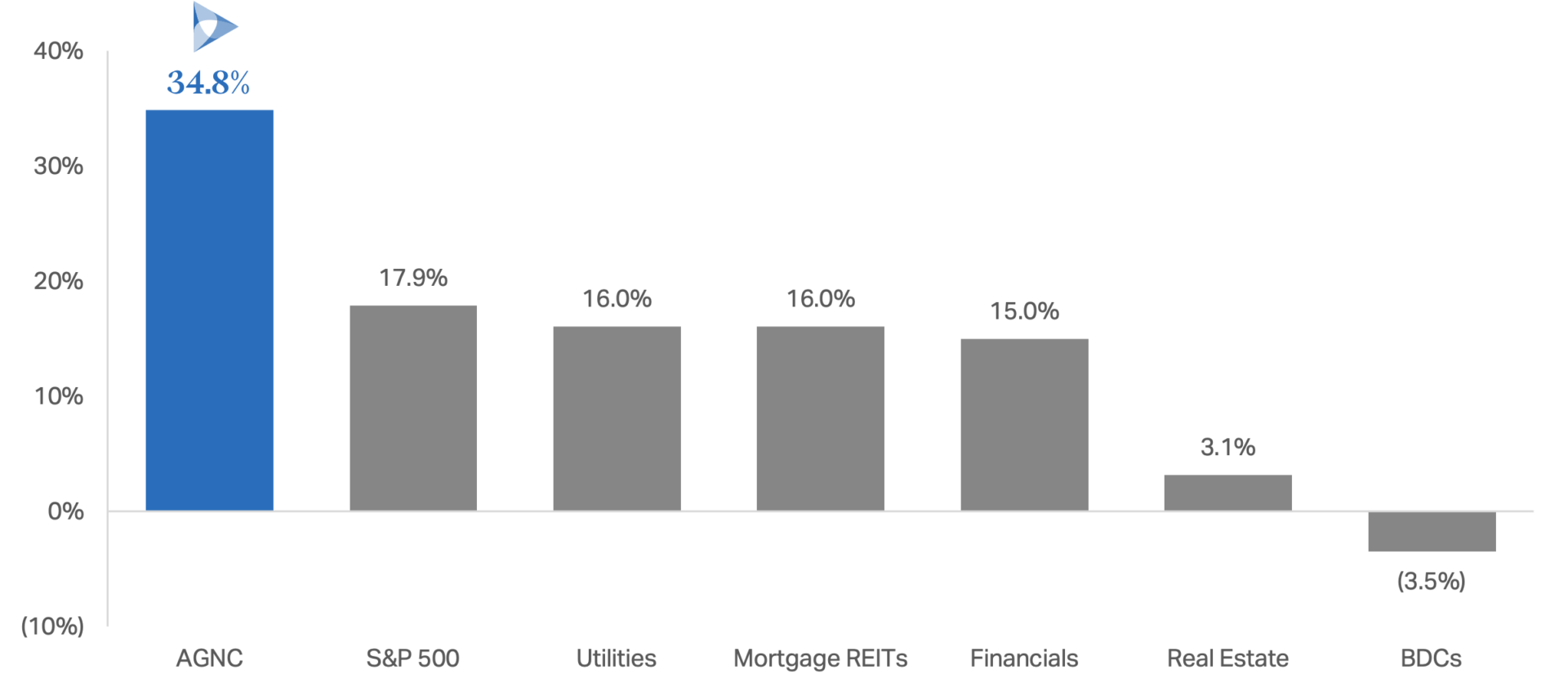

AGNC delivered exceptional results for stockholders in 2025, driven by strong Agency MBS performance and our specialized portfolio management strategies. For the year, AGNC generated an economic return of 22.7%, comprised of $1.44 of dividends per share and a $0.47 increase in tangible net book value per share. This performance represents AGNC’s best annual economic return since 2012 and the highest economic return among our Agency REIT Peer Group for the second consecutive year.1,2 Even more noteworthy, AGNC’s total stock return in 2025 was 34.8% with dividends reinvested, nearly doubling the S&P 500 Index and significantly outperforming major yield-oriented equity sectors.3

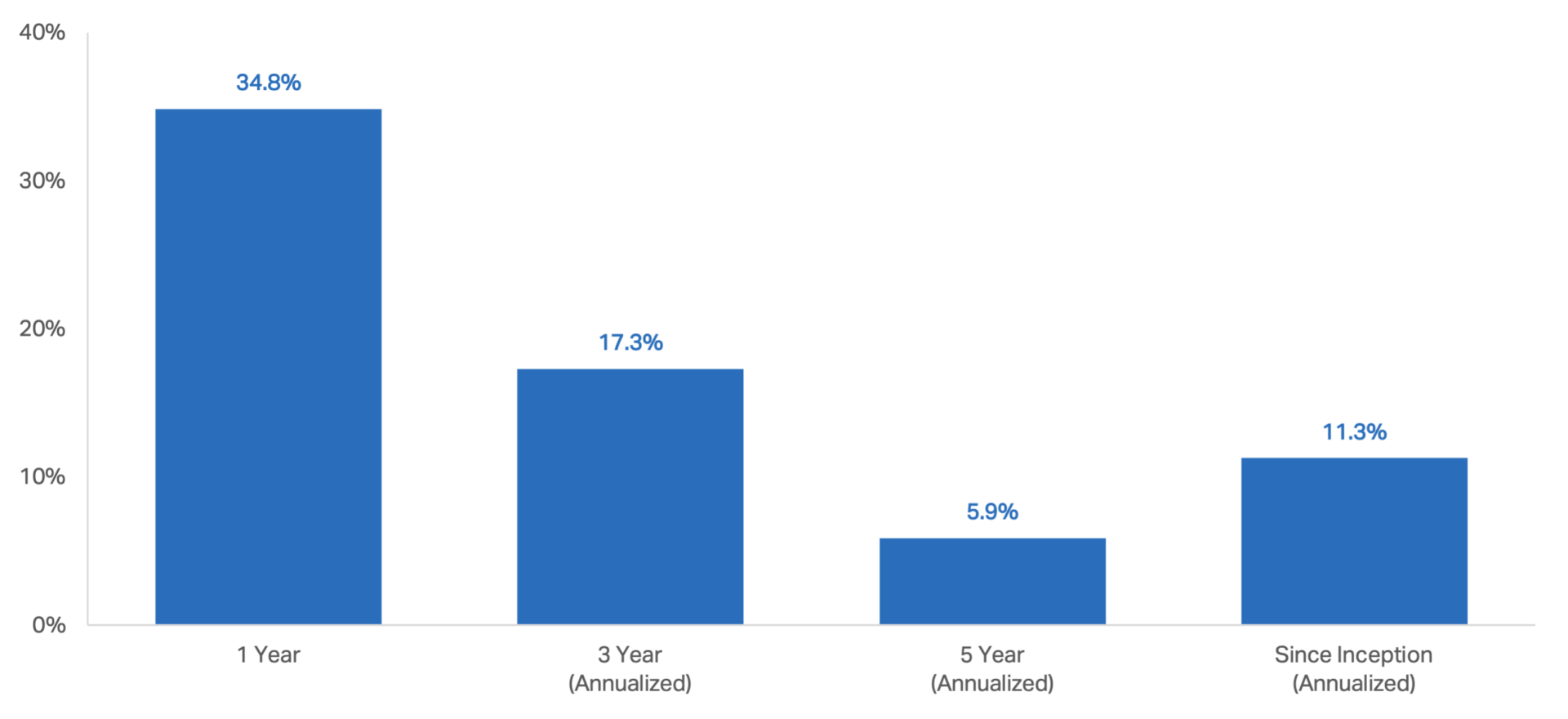

In 2025, AGNC generated the second best annual total stock return in the Company’s history, driven by an attractive dividend yield. Since inception, AGNC has delivered an annualized total stock return of 11.3%, outperforming each of its Agency-focused REIT peers over this period.3

2025 Total Stock Returns3

In late 2023, we expressed our belief that AGNC was at the forefront of a durable and attractive investment environment as the Fed’s unprecedented tightening cycle reached its conclusion. At that time, Agency MBS spreads to benchmark interest rates had begun to stabilize at historically wide levels, providing generationally attractive return opportunities for Agency MBS investors. That outlook proved to be correct. Despite several episodes of extreme market turbulence, including the U.S. presidential election in 2024 and the ‘Liberation Day’ tariff announcements in 2025, AGNC stockholders experienced an annualized total stock return of 23% from the end of the third quarter of 2023 through the end of 2025.3 On the heels of one of the best years in AGNC’s history from both a total stock and economic return perspective, many of the favorable fundamental and technical factors that drove AGNC’s 2025 performance remain intact and supportive of our positive outlook as we enter 2026.

AGNC Total Stock Returns3

(Measured over the trailing periods shown, each ended December 31, 2025)

A FAVORABLE MACROECONOMIC BACKDROP

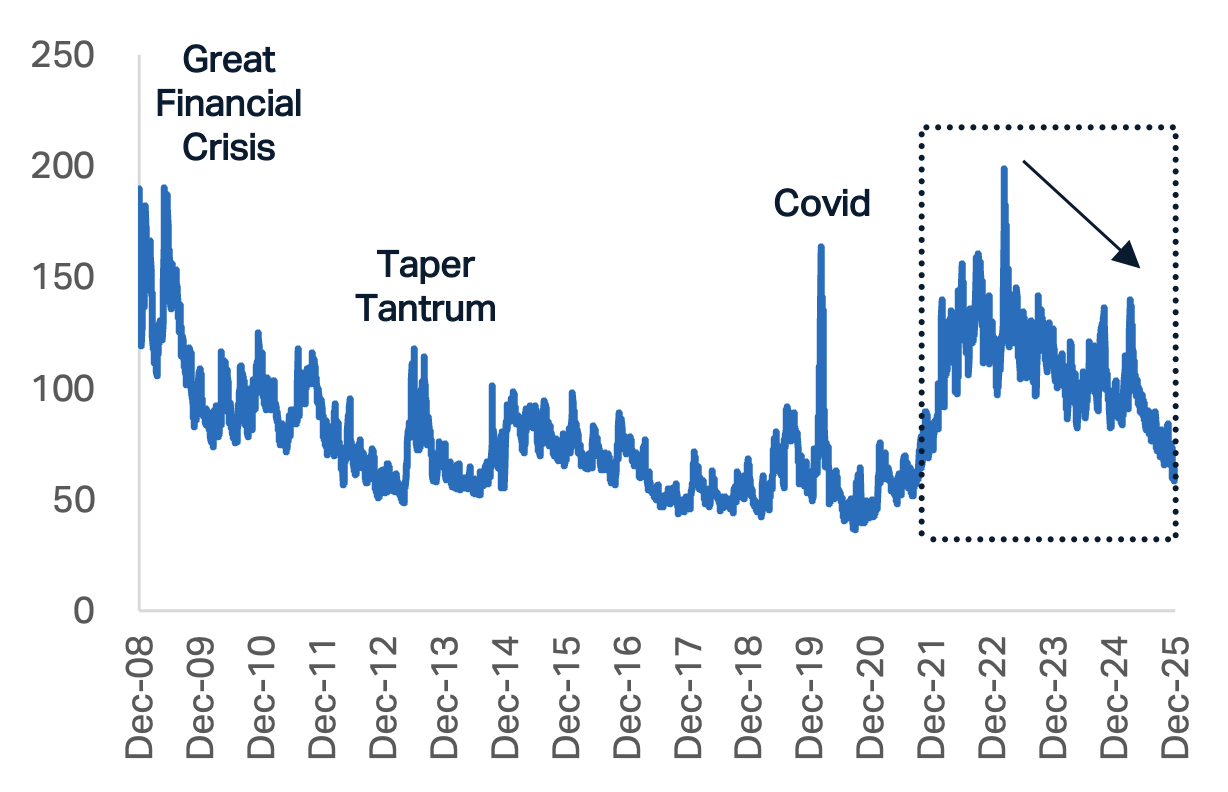

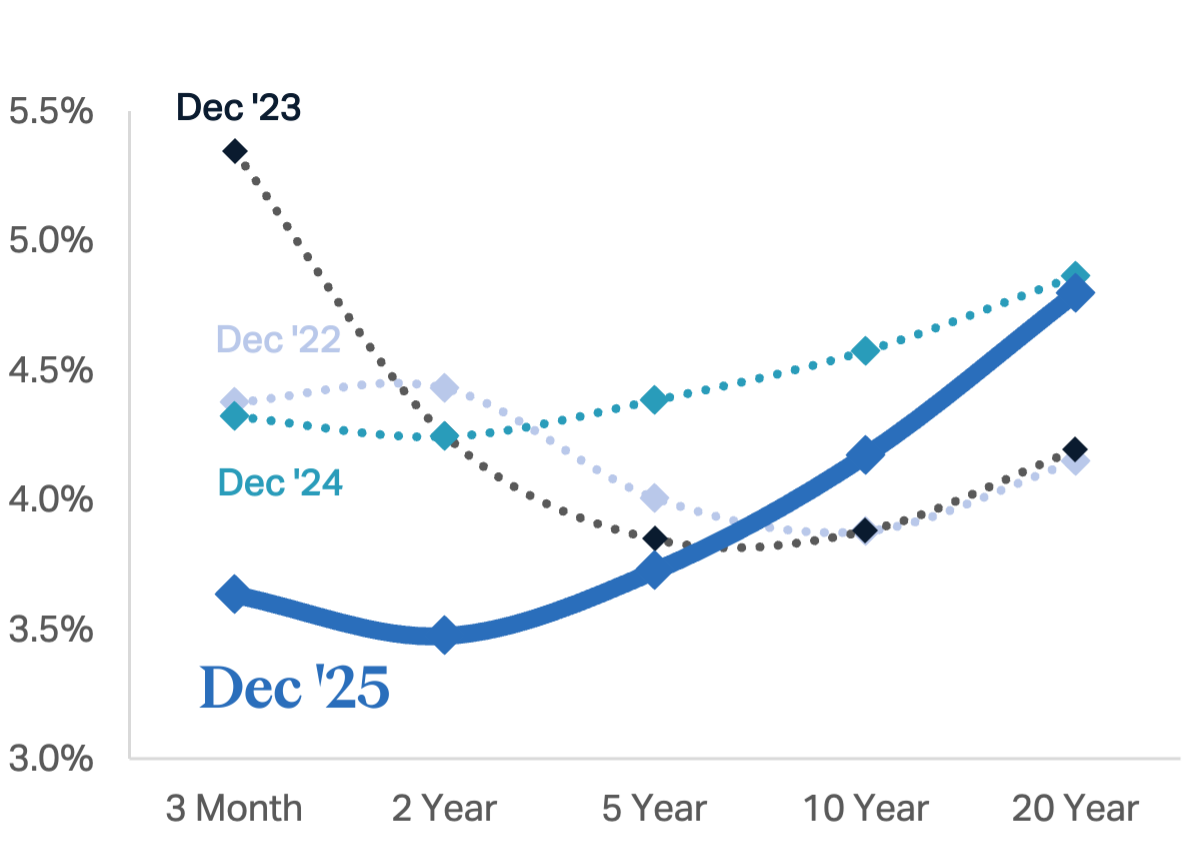

In 2025, Agency MBS benefited from a favorable macroeconomic climate, and investor sentiment continued to improve across the fixed income spectrum. From a monetary policy standpoint, the Fed continued on its gradual path to a neutral rate, delivering three interest rate cuts and reducing the federal funds rate by 75 basis points over the course of the year. As expected, the Fed also pivoted its balance sheet activity from quantitative tightening to reserve management as bank reserves reached an ‘ample’ level. Following the unprecedented 2022-2023 tightening cycle that combined aggressive interest rate hikes with significant balance sheet runoff, the Fed has now reduced the federal funds rate by 175 basis points since September 2024. This shift toward lower short-term rates and greater accommodation, along with greater fiscal policy clarity, a stable supply outlook for Treasury securities, and a greater anticipated share of short-term Treasury issuance, drove declines in interest rate volatility and a further steepening of the yield curve over the course of the year.

Interest Rate Volatility (MOVE Index)4

U.S. Treasury Yield Curve5

AGENCY MBS: STRONG 2025 PERFORMANCE

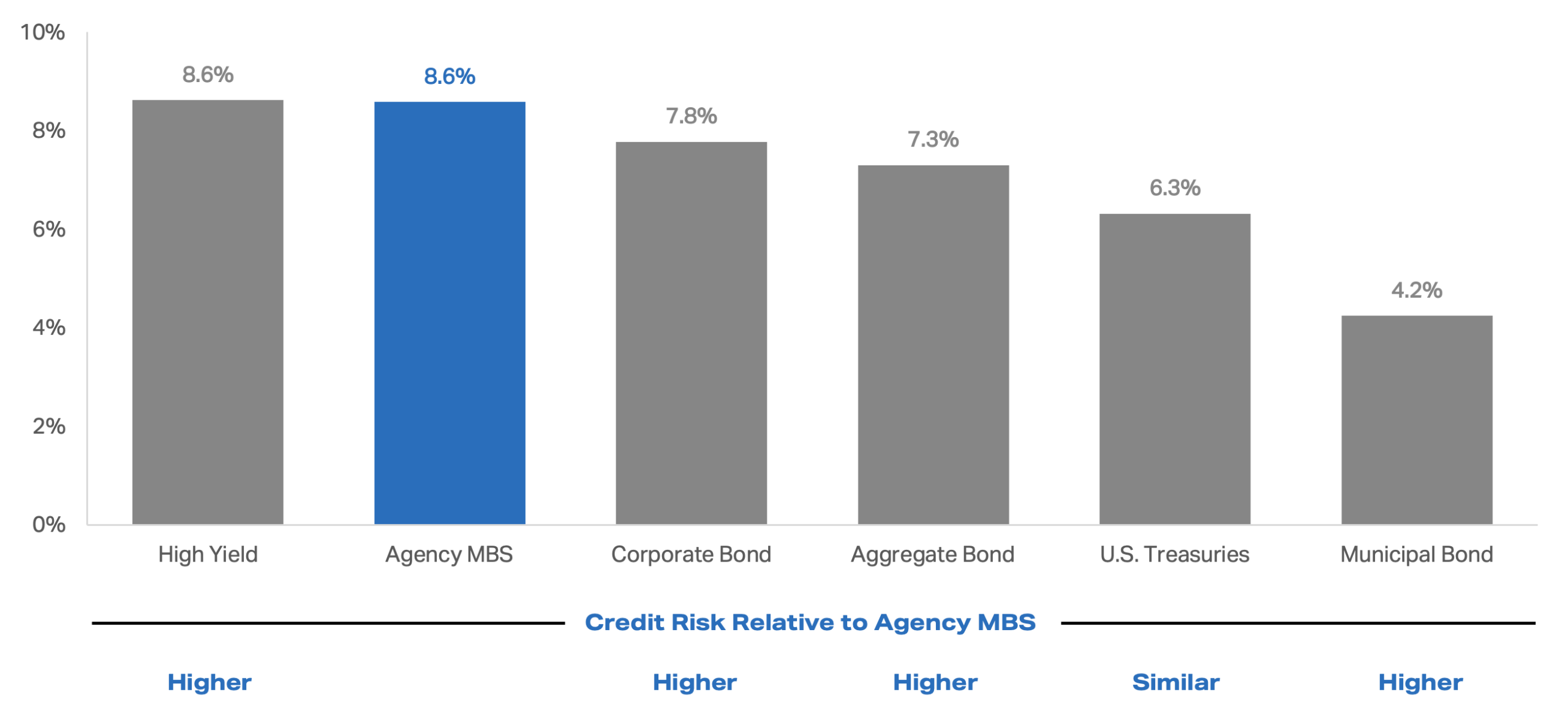

While this constructive monetary and fiscal policy backdrop supported strong returns across fixed income assets, the performance of Agency MBS was particularly notable. The Bloomberg Agency MBS Index produced an unlevered total return of 8.6% in 2025, its best annual return since 2002, and outperformed virtually all domestic fixed income sectors. Further, the Agency MBS Index significantly outpaced the U.S. Treasury Index, despite both asset classes possessing a similar credit profile.6

2025 Fixed Income Total Returns6

In addition to the supportive fixed income backdrop, several developments contributed to the meaningful outperformance of Agency MBS.

| Macro Theme | Development |

|---|---|

| Greater Clarity in Approach to GSE Reform | The uncertainty and potential risks related to the path of GSE reform that created an overhang on the Agency MBS market early in the year gradually diminished as the Administration signaled an approach focused on reducing Agency MBS spreads, maintaining mortgage market stability, and improving housing affordability. |

| Balanced Supply and Demand | The net new supply of Agency MBS was manageable, and total supply, inclusive of Fed runoff, was in-line with prior years. The Agency MBS investor base diversified further as private investor demand expanded, bank demand slowly returned, and the GSEs grew their retained portfolios in the later months of 2025. |

| Improved Funding Market Dynamics | The end of the Fed’s quantitative tightening cycle and renewed growth in the size of its balance sheet, coupled with improved functionality of its Standing Repo Program (SRP), eased short-term funding market pressures. |

| Attractive Agency MBS Spreads | Despite tightening from historically wide levels over the course of 2025, Agency MBS spreads to benchmark rates and, in turn, projected investment returns remained attractive on both an absolute basis and relative to other yield-oriented fixed income products that have credit risk, such as investment grade (IG) corporate bonds. |

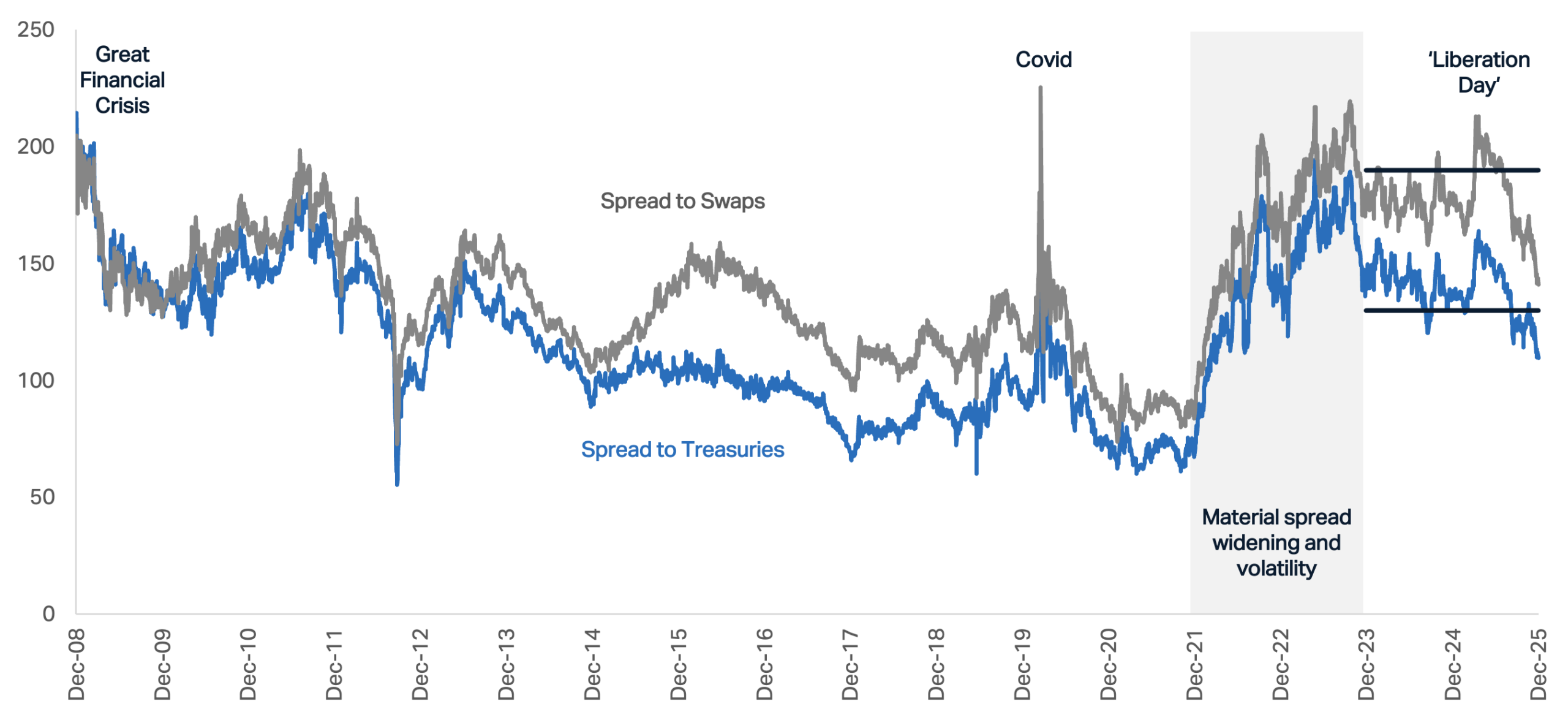

Agency MBS Spreads7

(Basis points)

Agency MBS: positive backdrop remains intact

Many of the favorable macro themes of 2025 remain in place and provide a constructive investment backdrop for AGNC’s business as we begin 2026.

| Macro Theme | Outlook |

|---|---|

| Interest Rate Environment | Favorable Interest rate volatility remains low and the yield curve steep by recent measures, providing a favorable interest rate environment for levered Agency MBS investors. |

| Federal Reserve Outlook | Balanced to Favorable The Fed is expected to continue to cut its benchmark federal funds rate, to the extent consistent with macroeconomic data, to its neutral level (expected to be 2.75–3.25%) over the course of the next year. Financial markets have largely accepted the nomination of Kevin Warsh as the next Fed Chair, eliminating another potential source of market volatility. |

| Administrative Focus on Housing Affordability and Potential GSE Reform | Favorable Commentary from the Administration, and the Treasury Department in particular, continues to prioritize housing affordability and a do-no-harm approach to the mortgage market. The January 2026 announcement directing the GSEs to purchase $200 billion of Agency MBS provides an example of the type of action that could result in tighter mortgage spreads and lower mortgage rates. |

| Supply and Demand Technicals | Balanced to Favorable Agency MBS supply is expected to remain manageable, and the investor base is positioned to expand. Private investor demand is expected to remain strong; bank demand could grow, particularly if favorable regulatory reforms are implemented; and GSE purchases could potentially consume about half of the supply in 2026. |

| Funding Market Dynamics | Favorable After taking action in 2025 to improve the functionality of the SRP, the Fed is considering other actions to further improve the SRP’s utility, such as clearing the SRP through the Fixed Income Clearing Corp. (FICC), and using a repo-based measure as its primary target rate. If implemented, these developments would be highly beneficial to the Agency MBS funding markets. |

| Agency MBS Spreads | Balanced to Favorable The downside risk of material mortgage spread widening appears much more limited relative to the last several years, particularly as the Administration remains focused on improving housing affordability through stable or tighter Agency MBS spreads. At current levels, Agency MBS spreads remain wide relative to long-term historical averages, offer favorable return opportunities on new investments, and provide attractive value relative to other fixed income investment alternatives. |

While bouts of financial market volatility are inevitable, the underlying fundamental and technical factors for Agency MBS continue to be favorable and supportive of our positive outlook.

AGNC: DIVERSIFICATION, YIELD, AND A PROVEN TRACK RECORD

Agency MBS assets benefit from compelling fundamentals and favorable attributes that we believe make them an important building block of any diversified investment portfolio. These assets offer tangible diversification advantages: minimal correlation to U.S. equities, U.S. Government support that substantially eliminates credit risk, and the opportunity to generate compelling current income across market cycles. AGNC provides stockholders access to the benefits of Agency MBS through a highly liquid portfolio that is actively managed by an expert team with decades of experience investing in this fundamental asset class.

BENEFITS OF INVESTING IN AGENCY MBS

DIFFERENTIATED ASSET

Fundamental fixed income asset class that supports the U.S. mortgage market with minimal correlation to equities

GOVERNMENT SUPPORT

Agency-backed guarantee from Fannie Mae, Freddie Mac, or Ginnie Mae substantially eliminates credit risk for investors

SUBSTANTIAL YIELD OPPORTUNITY

Compelling current income with an ability to employ leverage through highly attractive funding that enhances return potential

HIGHLY LIQUID MARKET

Massive fixed income asset class with substantial trading liquidity, second only to the U.S. Treasury market

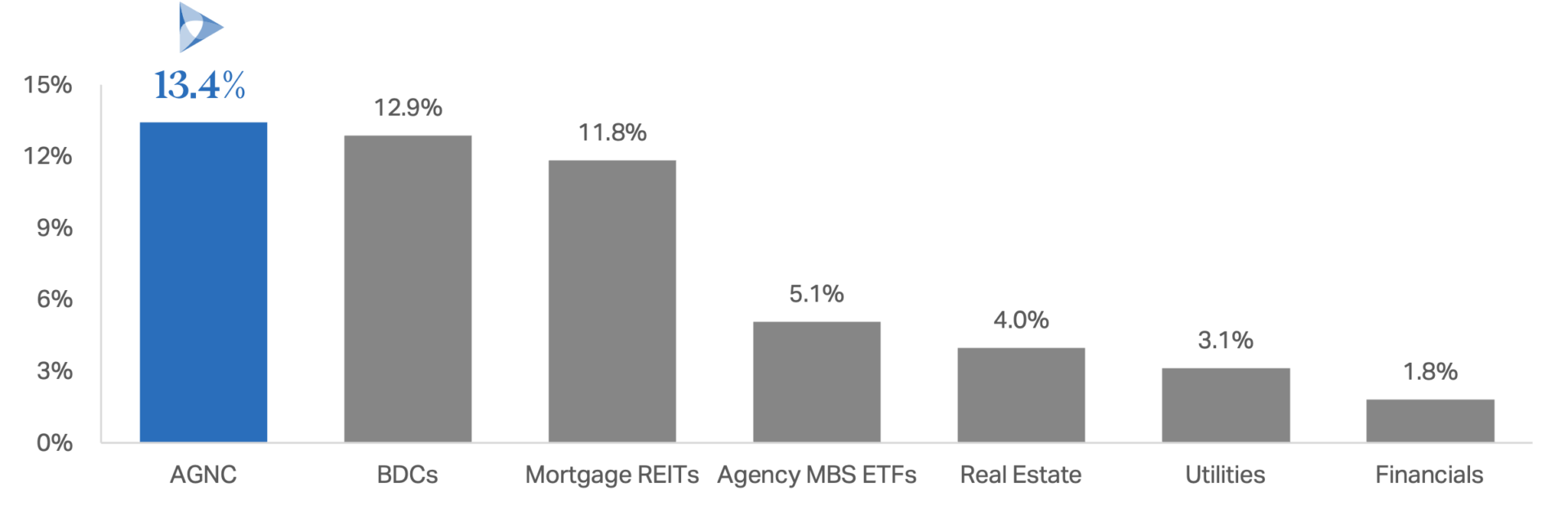

Our monthly common stock dividend, the main driver of our long-term returns, provides highly attractive current income to supplement an investor’s growth- or value-oriented portfolio. Notably, AGNC has paid over $15 billion of common stock dividends since inception, and our dividend yield meaningfully exceeds those of other traditional yield-oriented equity sectors and Agency MBS-centric models.

Dividend Yields8

Throughout our 18-year history, we have navigated a myriad of market cycles and exogenous events that have driven numerous periods of significant market volatility. Despite broad market turbulence, our levered and hedged portfolio of Agency MBS, coupled with our proven approach to mortgage investing, have generated highly attractive long-term returns on both an absolute and relative basis. Our exceptional performance in 2025 underscores the benefits of this proven approach, as AGNC outperformed the average Agency REIT Peer Group economic return by 11.7 percentage points for the year. Since inception, AGNC has outperformed this group by an average of 177 percentage points on a cumulative economic return basis.2 With a specialized focus on Agency MBS, our team’s ability to select high-quality assets, optimize financing, and dynamically manage interest rate and other market risks has created meaningful relative value for AGNC stockholders over the long run.

Our exceptional performance in 2025 underscores the benefits of our proven approach to mortgage investing, as AGNC outperformed the average Agency REIT Peer Group economic return by 11.7 percentage points for the year.2

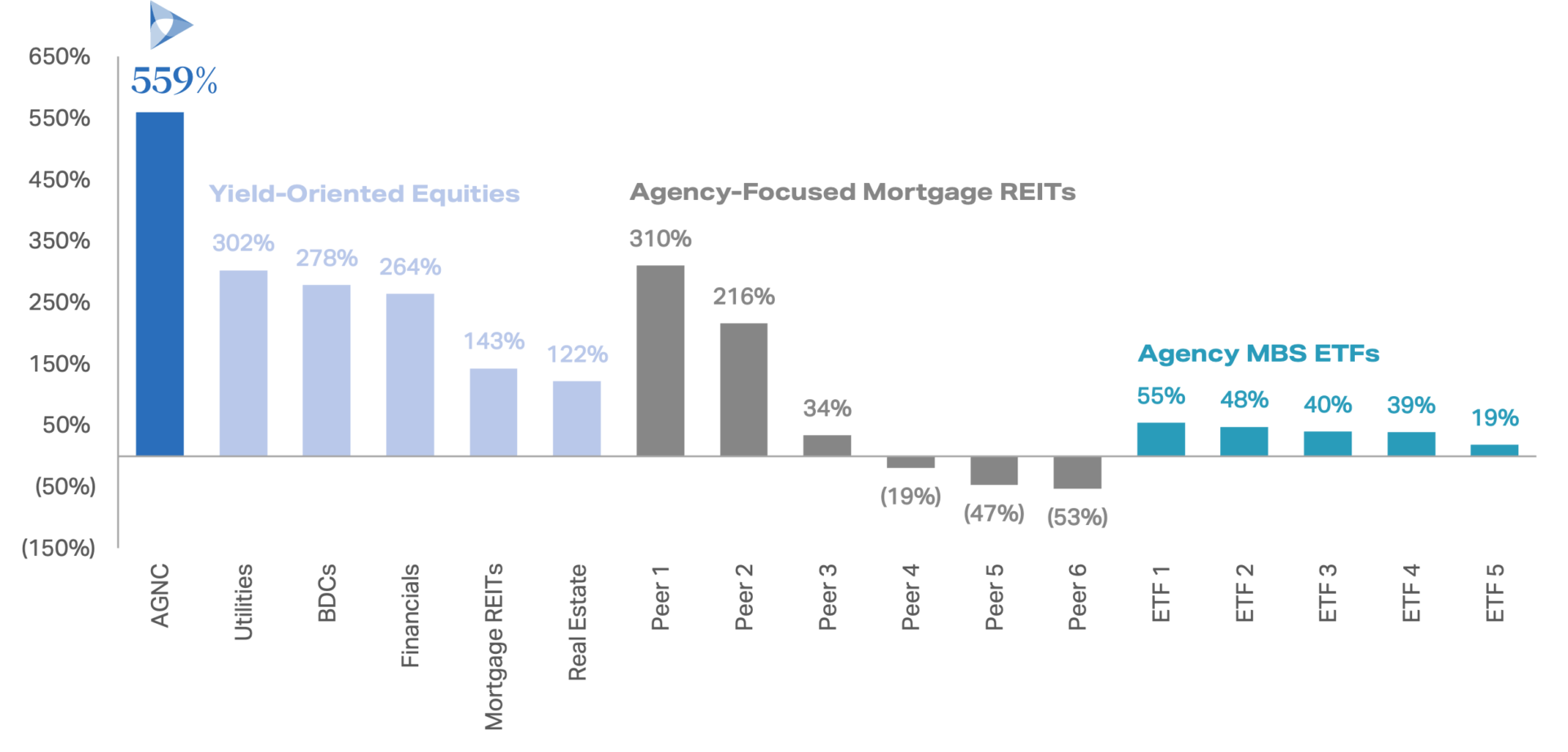

Since our inception in 2008, we have remained steadfastly focused on our primary objective: utilizing our Agency MBS investment expertise to generate favorable long-term stockholder returns with a substantial dividend yield component. Our long-term performance compares very favorably to yield oriented equity alternatives and other Agency MBS investment vehicles, demonstrating the resilience of our business model and the benefit of being a long-term investor in AGNC.

Total Stock Returns Since AGNC’s May 2008 IPO3

Further, AGNC’s stockholder-friendly attributes—an enduring commitment to responsible stewardship of our stockholders’ capital, industry-leading operating efficiency, significant scale, and a long-standing focus on transparency—have positioned AGNC as the best-in-class Agency MBS investor. Through an investment in AGNC, stockholders can access the powerful value of the AGNC franchise: a compelling combination of meaningful diversification benefits, highly attractive monthly dividend income, and a proven track record of favorable long-term risk-adjusted returns on both an absolute and relative basis.

As always, we appreciate your continued support of AGNC, and we wish you a healthy and prosperous 2026.

Best regards,

Peter J. Federico

President, Chief Executive Officer & Chief Investment Officer

February 20, 2026

ENDNOTES AND IMPORTANT NOTICES

1. Unless otherwise specified, all data in this letter is presented as of December 31, 2025.

2. When used in this letter, economic return is presented on a per common share basis and represents the sum of the change in tangible net book value per common share and dividends declared on common stock during the period over the beginning tangible net book value per common share. Where shown for comparison purposes, the Agency REIT Peer Group reflects an unweighted average of NLY, ARR, DX, IVR, ORC, and TWO. References to the one year or 2025 period are measured from December 31, 2024 through December 31, References to the ‘since inception’ period are measured from June 30, 2008 (the first quarter-end following AGNC’s May 2008 IPO) through December 31, 2025 and are shown on an absolute, unannualized basis; if a company was not publicly traded as of June 30, 2008, its economic return is measured beginning as of its first quarterly reporting date following the date it became publicly traded. Source: Company materials and filings.

3. Total stock return includes price appreciation and dividend reinvestment, and dividends are assumed to be reinvested at the closing price of the security on the ex-dividend date. Where shown, sectors reflect the following indices: BDCs (S&P BDC Index), Financials (S&P 500 Financials Index), Mortgage REITs (FTSE NAREIT Mortgage REITs Index), Real Estate (S&P 500 Real Estate Index), and Utilities (S&P 500 Utilities Index). Where shown for comparison purposes, Agency-focused residential mortgage REITs include Annaly Capital Management, Inc. (NLY), ARMOUR Residential REIT, Inc. (ARR), Dynex Capital, Inc. (DX), Invesco Mortgage Capital Inc. (IVR), Orchid Island Capital, Inc. (ORC), and Two Harbors Investment Corp. (TWO), and the Agency REIT Peer Group reflects an unweighted average of NLY, ARR, DX, IVR, ORC, and TWO. Where shown for comparison purposes, Agency MBS ETFs include First Trust Low Duration Opportunities ETF (LMBS), iShares MBS ETF (MBB), Janus Henderson Mortgage-Backed Securities ETF (JMBS), SPDR Portfolio Mortgage-Backed Bond ETF (SPMB), and Vanguard Mortgage-Backed Securities ETF (VMBS), and Agency MBS ETFs reflects an unweighted average of LMBS, MBB, JMBS, SPMB, and VMBS. References to the one year or 2025 period are measured from December 31, 2024 through December 31, 2025. References to the ‘since inception’ or ‘since IPO’ period are measured from AGNC’s May 2008 IPO through December 31, 2025. If a company or ETF shown was not publicly traded as of the date of AGNC’s May 2008 IPO, its total stock return is measured beginning as of the date it became publicly traded. Comparative data provided for informational purposes only. Past performance is not indicative of future results. An investment in AGNC involves different risks and uncertainties from indices, companies, and ETFs cited. Please refer to our annual report on Form 10-K and quarterly reports on Form 10-Q for a more complete description of the risks of our business. Source: Bloomberg.

4. MOVE Index reflects the ICE BofA Move Index from December 31, 2008 through December 31, 2025. Source: Bloomberg

5. U.S. Treasury yield curve reflects month-end Treasury yields for each tenor and month shown. Source: Bloomberg.

6. Fixed income sectors reflect the following indices: Agency MBS (Bloomberg U.S. MBS Index), Aggregate Bond (Bloomberg U.S. Agg Index), Corporate Bond (Bloomberg U.S. Corporate Bond Index), High Yield (Bloomberg U.S. Corporate High Yield Bond Index), Municipal Bond (Bloomberg U.S. Municipal Index), and U.S. Treasuries (Bloomberg U.S. Treasury Index). Total returns are measured from December 31, 2024 through December 31, 2025. Source: Bloomberg.

7. Agency MBS spread to U.S. Treasuries and Agency MBS spread to swaps reflect the 30-year current coupon Agency MBS yield spread to a 50/50 average of 5- and 10-year U.S. Treasury yields and a 50/50 average of 5- and 10-year SOFR OIS swaps, respectively, from December 31, 2008 through December 31, 2025. Source: Bloomberg.

8. Dividend yields as of December 31, 2025. Sectors shown reflect the following indices: BDCs (S&P BDC Index), Financials (S&P 500 Financials Index), Mortgage REITs (FTSE NAREIT Mortgage REITs Index), Real Estate (S&P 500 Real Estate Index), and Utilities (S&P 500 Utilities Index). Agency MBS ETFs reflects an unweighted average of LMBS, MBB, JMBS, SPMB, and VMBS. Comparative data provided Post for informational purposes only. Past performance is not indicative of future results. An investment in AGNC involves different risks and uncertainties from indices, companies, and ETFs cited. Source: Bloomberg.

IMPORTANT NOTICES: “AGNC,” the “Company,” “we,” “us,” or “our” refers to AGNC Investment Corp. This Annual Report contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act. Forward-looking statements are based on estimates, projections, beliefs and assumptions of management of the Company at the time of such statements and are not guarantees of future performance. As further described in the Management Discussion and Analysis included in this Annual Report, forward-looking statements involve risks and uncertainties in predicting future results and conditions. Actual results could differ materially from those projected in these forward-looking statements or from our historic performance due to a variety of important factors.

We use our website, AGNC.com, and LinkedIn and X accounts, linkedin.com/company/agnc-investment-corp and x.com/AGNCInvestment, to distribute information about the Company. Investors should monitor these channels in addition to our press releases, SEC filings, and public conference calls and webcasts, as information posted through them may be deemed material. Investors may also sign up to receive news, perspectives, SEC filing, and other types of email alerts at investors.agnc.com/shareholder-services/email-alerts. Our website, any alerts, and social media channels are not incorporated by reference into, and are not a part of, this document or any report filed with the SEC.