monthly macro monitor

key trends for the agency mbs investor

AUGUST 2025

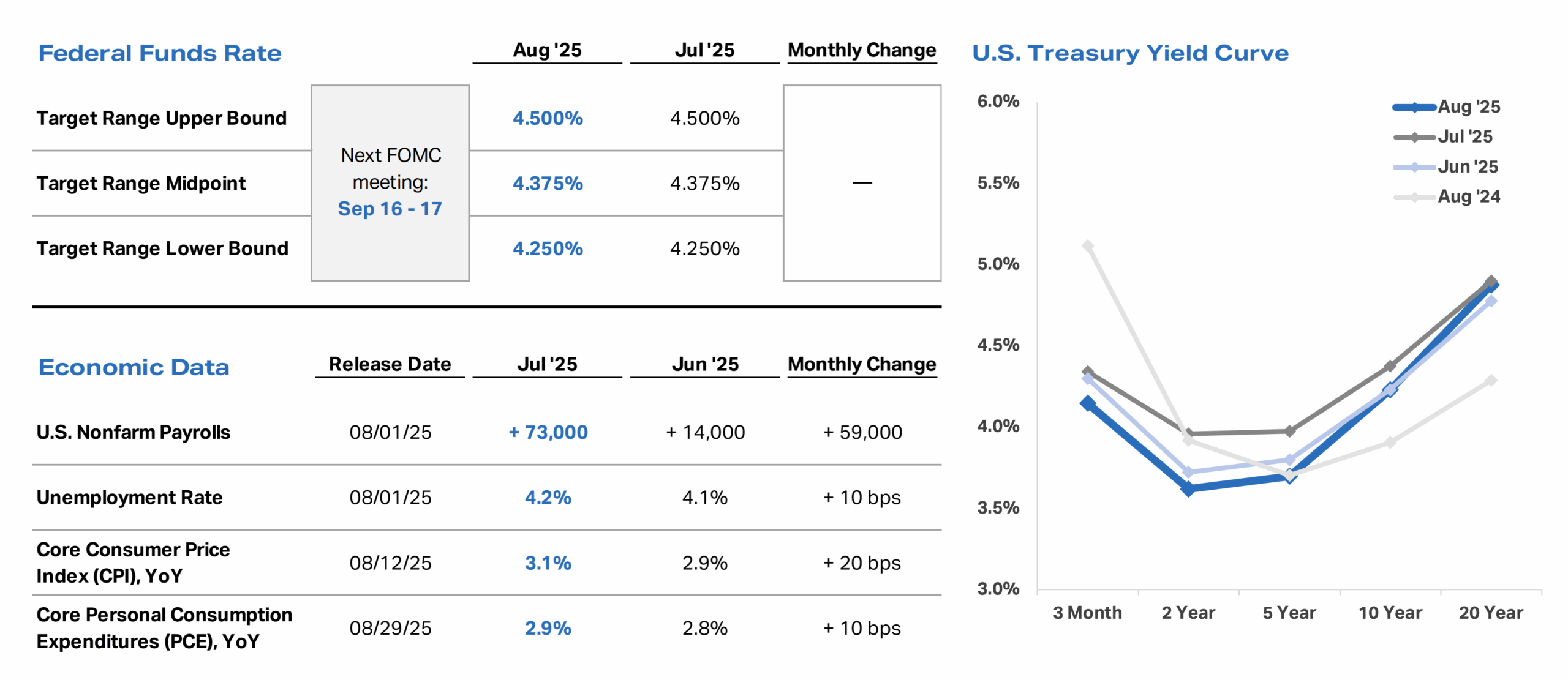

- The labor market showed signs of softening in August as July nonfarm payrolls missed consensus estimates and the previously reported May and June nonfarm payroll levels were revised meaningfully lower. While the unemployment rate also increased slightly, it was in line with estimates and has remained relatively stable over the past year.

- The impact of higher tariffs began to appear in the economic data and caused inflation measures to increase month-over-month. During his recent speech at the Jackson Hole symposium, Chair Powell noted that the Fed expects to see the effects of tariffs “accumulate over the coming months, with high uncertainty about timing and amounts.” He also stated that “a reasonable base case is that the effects will be relatively short-lived – a one-time shift in the price level” but cautioned that “one-time does not mean all at once.”

- Considering these economic data developments, Chair Powell also indicated a potential near-term shift in the Fed’s monetary policy stance, and market participants are now widely expecting a 25 basis point rate cut at the September meeting.

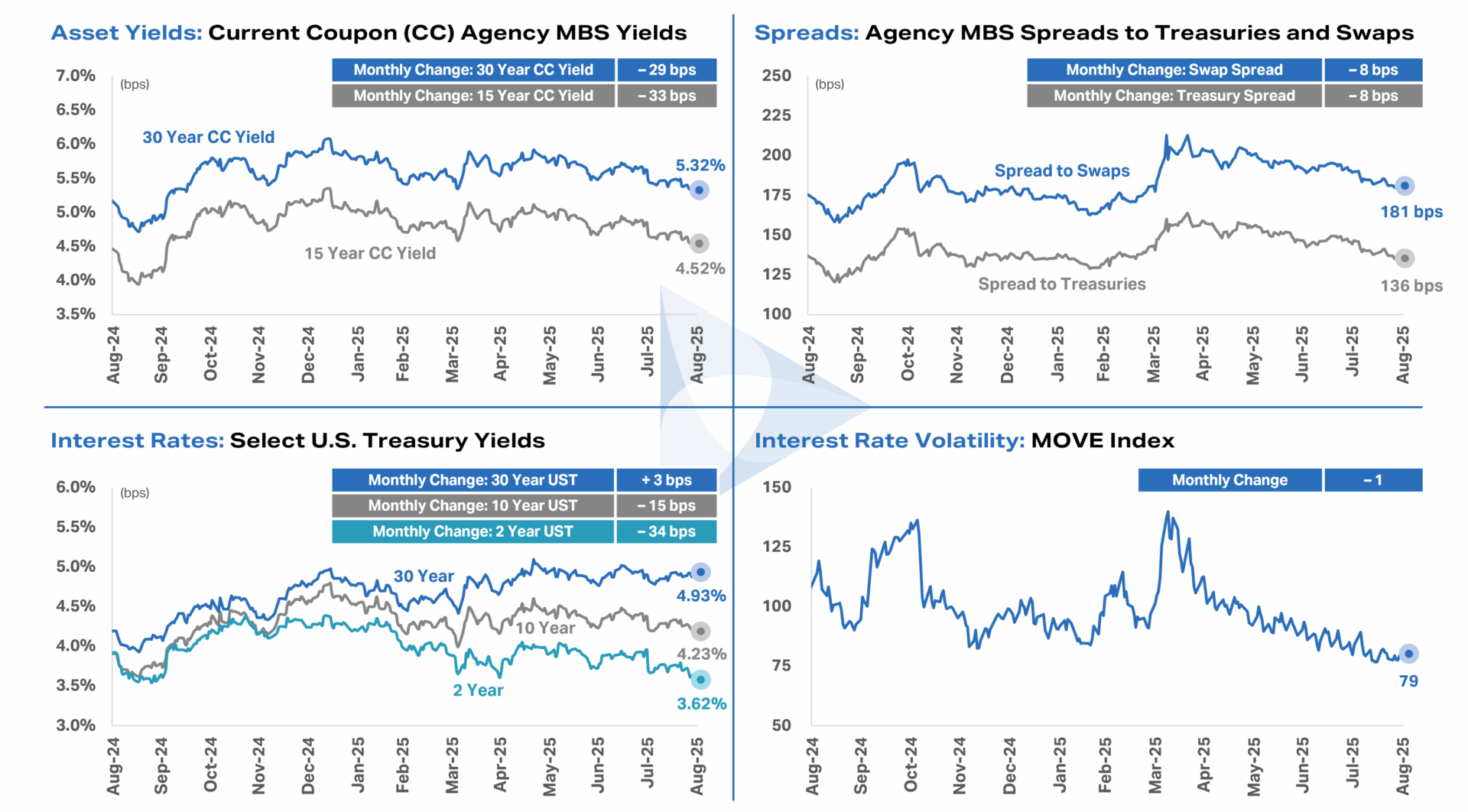

- Against the backdrop of increasing rate cut expectations, benchmark interest rates generally declined, the yield curve steepened, and Agency MBS spreads to benchmark rates tightened during the month. Further, interest rate volatility remained relatively subdued in August, an incremental positive for Agency MBS investors.

Key Rate and Spread trends

Important Disclosures

Federal funds rate data last updated August 31, 2025. Source: Federal Reserve.

Economic data last updated August 31, 2025. Core CPI and Core PCE exclude food and energy. Source: Bureau of Labor Statistics and Bureau of Economic Analysis.

U.S. Treasury yield curve reflects month-end Treasury yields for each tenor and month shown. Source: Bloomberg.

Agency MBS spread to U.S. Treasuries and Agency MBS spread to swaps reflect the 30-year current coupon Agency MBS yield spread to a 50/50 average of 5- and 10-year U.S. Treasury yields and a 50/50 average of 5- and 10-year SOFR OIS swaps, respectively. MOVE Index reflects the ICE BofA Move Index. Each chart is shown over the trailing 12 months ended August 31, 2025, and each monthly change (rounded to the nearest whole number) reflects the difference between August 2025 month-end data and July 2025 month-end data. Source: Bloomberg.

Data and commentary, including thoughts, opinions, and outlook of AGNC Investment Corp. (“AGNC”) management, are provided for information purposes only and should not be construed as investment advice.

Investment in AGNC involves risks and uncertainties that may cause future performance to vary from historical results or any forward-looking commentary provided. Please refer to our annual and quarterly reports on file with the SEC and available on our website or at www.sec.gov for more information about AGNC, including material risks, other factors that may affect future performance, and notices regarding forward-looking statements. AGNC disclaims any obligation to update or revise any forward-looking commentary. Stockholders and other interested parties may sign up to receive AGNC’s news, perspectives, and other types of email alerts by clicking the Subscribe link below.