monthly macro monitor

key trends for the agency mbs investor

JANUARY 2026

- Following the shutdown-related delays in late 2025, economic data reporting largely returned to schedule in January with the exception of PCE data, which remains on a lag with December figures expected to be released in February. Despite potential timing distortions in the data, Chair Powell characterized the tension in the Fed’s dual mandate of maximum employment and price stability as having eased slightly at his January press conference as the upside risks to inflation and the downside risks to employment have both diminished somewhat.

- As generally expected, the FOMC maintained the target range for the federal funds rate at 3.50-3.75% at its January meeting, following three consecutive interest rate cuts in September, October, and December. Fed funds futures are currently pricing in a high probability of two interest rate cuts in 2026, as compared to the median expectation of one cut indicated in the Fed’s December Summary of Economic Projections (SEP).

- At the end of the month, President Trump nominated Kevin Warsh, who previously served on the Fed Board of Governors from 2006-2011, to succeed Jerome Powell as the next Fed Chair. While Powell’s term on the Fed Board of Governors extends through January 2028, his term as Chair ends in May 2026. He has thus far declined to comment on whether he plans to remain on the Board of Governors following the end of his term as Chair.

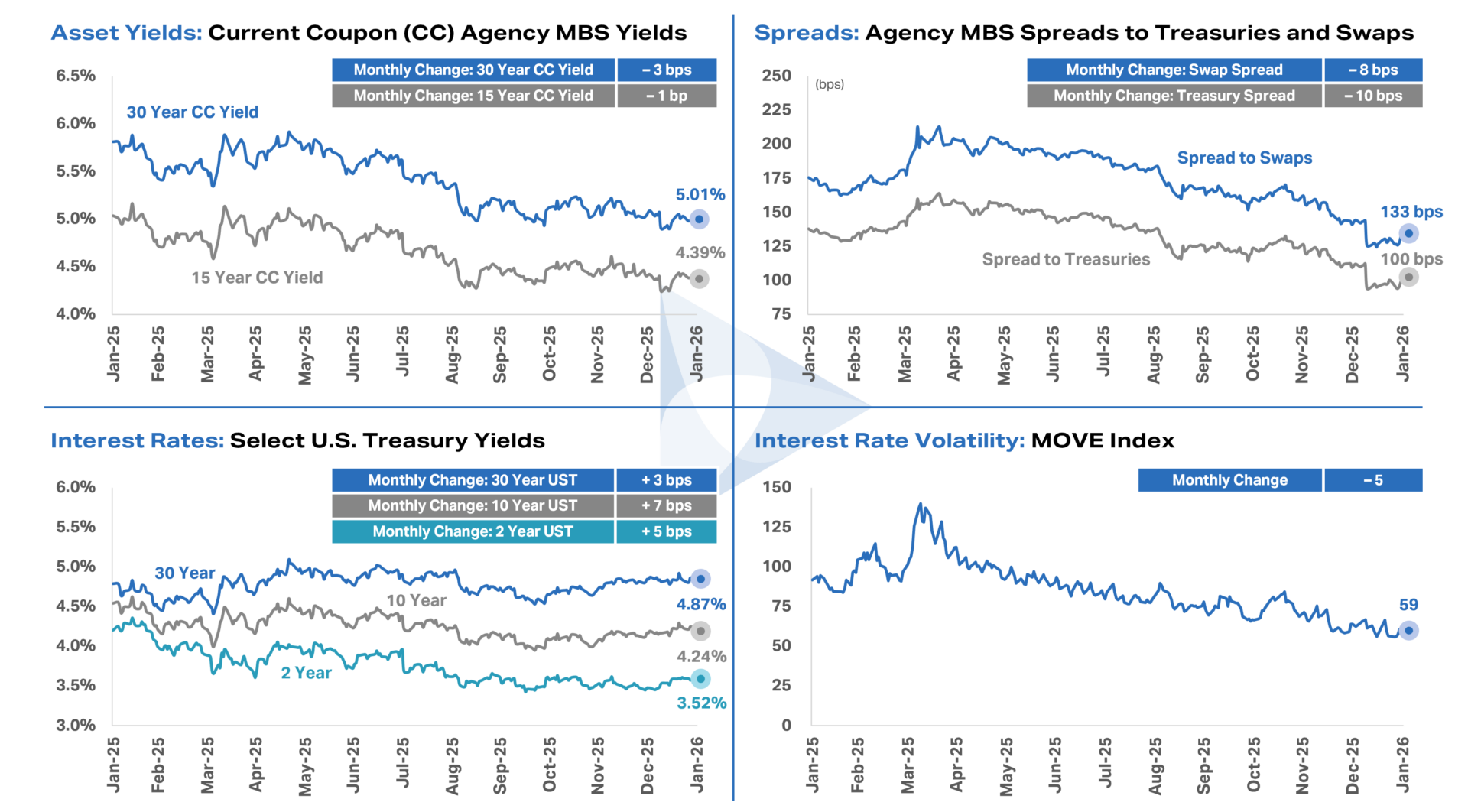

- Following a strong 2026, the macro environment for Agency MBS remained favorable in January, as interest rate volatility declined and Agency MBS spreads to benchmark rates tightened over the course of the month. President Trump’s announcement early in the month directing Fannie Mae and Freddie Mac (the GSEs) to purchase $200 billion of Agency MBS caused spreads to tighten sharply, but his nomination of Warsh drove moderate spread widening at the end of the month and offset some of the benefit of the GSE MBS purchase announcement.

Key Rate and Spread trends

Important Disclosures

Federal funds rate data last updated January 31, 2026. Source: Federal Reserve.

Economic data last updated January 31, 2026. Core CPI and Core PCE exclude food and energy. Source: Bureau of Labor Statistics and Bureau of Economic Analysis.

U.S. Treasury yield curve reflects month-end Treasury yields for each tenor and month shown. Source: Bloomberg.

Agency MBS spread to U.S. Treasuries and Agency MBS spread to swaps reflect the 30-year current coupon Agency MBS yield spread to a 50/50 average of 5- and 10-year U.S. Treasury yields and a 50/50 average of 5- and 10-year SOFR OIS swaps, respectively. MOVE Index reflects the ICE BofA Move Index. Each chart is shown over the trailing 12 months ended January 31, 2026, and each monthly change (rounded to the nearest whole number) reflects the difference between January 2026 month-end data and December 2025 month-end data. Source: Bloomberg.

Data and commentary, including thoughts, opinions, and outlook of AGNC Investment Corp. (“AGNC”) management, are provided for information purposes only and should not be construed as investment advice.

Investment in AGNC involves risks and uncertainties that may cause future performance to vary from historical results or any forward-looking commentary provided. Please refer to our annual and quarterly reports on file with the SEC and available on our website or at www.sec.gov for more information about AGNC, including material risks, other factors that may affect future performance, and notices regarding forward-looking statements. AGNC disclaims any obligation to update or revise any forward-looking commentary. Stockholders and other interested parties may sign up to receive AGNC’s news, perspectives, and other types of email alerts by clicking the Subscribe link.