THE EARNINGS Extract

Q1 2026 EARNINGS COMMENTARy

APRIL 21, 2026

Agency MBS performance in the first quarter was driven by two divergent macroeconomic themes. In January and February, the administration’s focus on reducing interest rate volatility, maintaining mortgage spread stability, and improving housing affordability drove strong performance across the broader fixed income complex and Agency MBS specifically. This favorable investment environment was, however, quickly eclipsed in March by the war in Iran and the potential for more widespread conflict in the Middle East. The associated increase in volatility and negative shift in investor sentiment caused Agency MBS spreads to benchmark rates to widen, and, as a result, AGNC’s economic return on tangible common equity in the first quarter was (1.6)%. Despite the quarter-over-quarter spread widening, Agency MBS generated a positive excess return to both U.S. Treasuries and investment grade corporate bonds in the first quarter, again demonstrating the diversification benefit of this high credit quality, fixed income asset class.

We continue to believe that many of the factors we cited at the beginning of the year remain positive catalysts for Agency MBS performance. First, mortgage spreads to benchmark rates widened significantly in March and provide investors with compelling value on both an absolute and relative basis at these levels. Second, supply-demand technicals have improved as a result of higher mortgage rates, increased bond fund inflows, and proposed regulatory capital changes. Third, the higher rate environment also increases the likelihood of actions by the administration to stabilize or reduce mortgage spreads as a means to mitigate housing affordability issues. Finally, although interest rate volatility has increased and the path of future Federal Reserve monetary policy actions has become a bit more uncertain, we believe that, with some form of resolution or easing of tensions in the Middle East, these factors could quickly revert to positive catalysts for Agency MBS. As a result, our longer-term outlook for Agency MBS remains constructive, despite near-term challenges associated with heightened geopolitical and macroeconomic risks. Moreover, AGNC is well-positioned to capitalize on these favorable conditions and build upon our lengthy track record of generating strong risk-adjusted returns over market cycles for our stockholders.

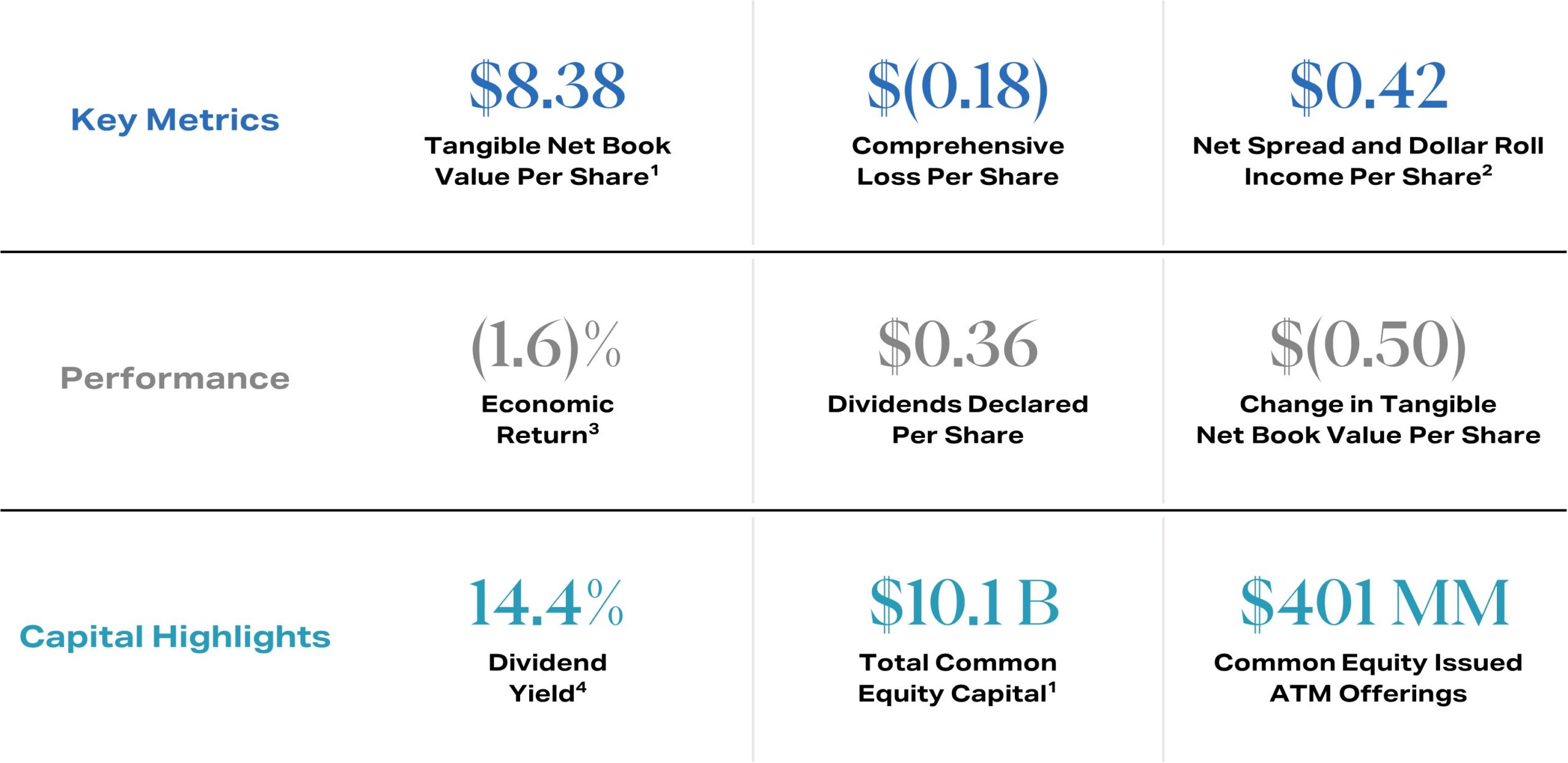

Q1 2026 Highlights

management commentary highlights

Macroeconomic and Agency MBS Market Environment

Peter Federico | President, Chief Executive Officer, and Chief Investment Officer

Agency MBS performance in the first quarter was driven by two very divergent investment themes. In January and February, the administration’s focus on reducing interest rate volatility, maintaining mortgage spread stability, and improving housing affordability drove strong performance across the fixed income markets. Agency MBS performance was particularly strong during this period, as President Trump’s January 8th directive instructing the GSEs to purchase $200 billion of Agency MBS pushed spreads through the lower end of the recent three-year trading range. In March, however, uncertainty associated with the war in Iran and the potential for a more widespread conflict in the Middle East caused interest rate volatility to increase, investor sentiment to turn negative, and Agency MBS spreads to widen significantly. As a result, AGNC’s economic return in the first quarter was (1.6)%. Despite the spread widening to swaps quarter-over-quarter, Agency MBS outperformed U.S. Treasuries and investment grade corporate bonds in the first quarter, again demonstrating the diversification benefit of this unique, high credit quality, fixed income asset class.

At the beginning of the year, we discussed a number of factors that we believed would benefit Agency MBS performance in 2026. Among these were low interest rate volatility and an accommodative monetary policy stance. In the first quarter, however, the Middle East conflict caused interest rate volatility to increase and Fed rate cuts to become more uncertain. While the duration and economic implications of the conflict are still unknown, recent developments are encouraging, and these factors could once again be positive catalysts for Agency MBS performance.

More importantly, many of the other factors that we discussed improved in the first quarter and now further strengthen the outlook for Agency MBS. Most notably, at current spread levels, the return profile on Agency MBS is more attractive. At the time of our fourth quarter of 2025 earnings call, the spread differential between current coupon Agency MBS and a blend of swaps was approximately 135 basis points. Over the last two months, that spread has ranged between 150 and 175 basis points as a result of heightened geopolitical and macroeconomic risks. We believe Agency MBS, in this spread range, represent compelling value on both an absolute and relative basis.

The supply outlook for Agency MBS also improved in the first quarter. At the start of the year, the net new supply of Agency MBS was expected to be approximately $250 billion, assuming a mortgage rate of just below 6%. With mortgage rates now about 50 basis points higher, MBS supply could be $50 to $70 billion lower this year. The demand outlook for Agency MBS improved in the first quarter as well. Money manager demand for Agency MBS increased materially in the first quarter as bond fund inflows came in about double the pace of the previous two years. U.S. bank regulators also released their proposed bank regulatory capital framework for comment. As expected, the proposal includes lower capital requirements for high quality mortgage credit. These favorable capital requirements could lead banks to retain a greater share of mortgage credit in whole loan form or to utilize the private label securitization path to a greater extent, thereby reducing the GSE footprint over time.

Finally, with mortgage spreads wider and the mortgage rate now in the low to mid-6% range, the administration may take further actions to improve housing affordability. Such actions could include more aggressive GSE purchases or increases in GSE portfolio size limits. Either or both of these actions would benefit mortgage performance. In addition, while the funding markets for Agency MBS are deep and liquid, further actions by the Fed to improve the functionality and accessibility of the standing repo program could also be catalysts for tighter mortgage spreads and lower mortgage rates.

In summary, although the sharp increase in geopolitical and macroeconomic risk creates a more challenging investment environment over the near term, the return profile and technical backdrop for Agency MBS improved in the first quarter. In addition, actions by the administration to improve housing affordability are more likely. As we are continually reminded, market conditions change quickly. A prompt resolution to the Middle East conflict, while at times difficult to predict, could lead to a substantial reduction in volatility and inflationary pressures. Collectively, these conditions support our favorable outlook for Agency MBS. Moreover, AGNC remains well-positioned to capitalize on these favorable conditions and build upon our lengthy track-record of generating strong risk-adjusted returns for our stockholders over a wide range of market cycles.

Our Quarterly Financial Results

Bernie Bell | EVP and Chief Financial Officer

For the first quarter of 2026, AGNC reported a comprehensive loss of $(0.18) per common share. Our economic return on tangible common equity was (1.6)% for the quarter, consisting of $0.36 of dividends declared per common share and a $(0.50) decrease in tangible net book value per share, driven by wider mortgage spreads to benchmark rates. As of late last week, our tangible net book value per common share was up approximately 6% for April, or approximately 5% net of our monthly dividend accrual. With the recovery in April through the end of last week, our tangible net book value has now largely reversed the first quarter decline.

We ended the first quarter with leverage of 7.4x tangible equity, up slightly from 7.2x as of the end of the fourth quarter of 2025, while average leverage for the quarter was unchanged at 7.4x tangible equity. We also ended the quarter with a significant liquidity position of $7.0 billion of unencumbered cash and Agency MBS, representing 60% of tangible equity.

Net spread and dollar roll income was $0.42 per common share for the quarter, up $0.07 from the fourth quarter of 2025. The increase was largely due to a 25 basis point increase in our net interest spread, which was driven by a combination of a greater allocation of interest rate swaps in our hedge portfolio, lower repo funding costs, more favorable TBA implied financing levels, and a modest increase in the yield on our asset portfolio. Our quarter-over-quarter results also benefited from reduced compensation expenses, as our fourth quarter of 2025 results included year-end incentive compensation accrual adjustments.

The average projected life CPR of our portfolio increased 70 basis points to 10.3% at quarter-end from 9.6% as of the fourth quarter. The increase was largely due to prepayment model updates implemented in the first quarter and portfolio composition changes, partly offset by higher mortgage rates. Actual CPRs averaged 13.2% for the quarter, compared to 9.7% in the prior quarter.

Lastly, during the first quarter, we issued $401 million of common equity through our at-the-market offering program at a significant premium to tangible net book value per share, continuing our active capital management strategy and generating meaningful accretion for our common stockholders.

Portfolio Update and Additional Commentary

Peter Federico | President, Chief Executive Officer, and Chief Investment Officer

Agency MBS performance varied meaningfully by coupon and hedge type in the first quarter. Low coupon MBS meaningfully outperformed high coupon MBS, due to heavy index buying from money managers in response to outsized bond fund inflows. This variation in performance by coupon was significant, with lower coupon MBS tightening about 10 basis points to Treasuries during the quarter, while higher coupon MBS widened about five basis points on average.

MBS performance also varied materially by hedge type as swap spreads tightened during the quarter. 10-year swap spreads, for example, tightened by almost 10 basis points. As a result, an Agency MBS position hedged with a 10-year pay-fixed swap versus a 10-year Treasury experienced spread widening of about 10 basis points, all else equal. This tightening in swap spreads was directly related to Middle East conflict uncertainty.

The market value of our portfolio totaled $94.7 billion at quarter-end. During the quarter, we purchased $1.7 billion of predominantly low-coupon specified pools. In addition, we rotated a portion of our portfolio down in coupon. Consistent with these changes, the weighted average coupon on our portfolio declined to 4.95% from 5.12% the prior quarter, and the percentage of assets with favorable prepayment characteristics increased slightly to 77%.

The notional balance of our hedge portfolio increased to approximately $64 billion due to the addition of shorter term pay-fixed swaps prior to the sharp selloff in interest rates in March. We also reduced our exposure to Treasury-based hedges during the quarter. As a result, in duration dollar terms, our swap hedge allocation increased to 78% from 70% the prior quarter. Lastly, in the current environment, we continue to favor operating with a positive duration gap, which we view as additional prepayment protection in a down rate scenario.

Important Disclosures

This commentary includes excerpts from AGNC Investment Corp.’s (“AGNC”) Q1 2026 earnings call. Click here to listen to the full webcast and access the earnings release and presentation.

Per share amounts are per share of common stock, unless otherwise indicated. Income and loss per share amounts are per diluted common share, unless otherwise indicated.

1. As of March 31, 2026. Tangible Net Book Value Per Share is net of the preferred stock liquidation preference and excludes goodwill.

2. Net Spread and Dollar Roll Income Per Share represents a non-GAAP measure. Refer to our Q1 2026 Stockholder Presentation for a reconciliation and further discussion of non-GAAP measures.

3. Economic Return represents the sum of the change in tangible net book value per common share and dividends declared on common stock during the period over the beginning tangible net book value per common share.

4. Dividend Yield as of March 31, 2026.

These materials contain forward-looking statements within the meaning of the Private Securities Litigation Reform Act. Forward-looking statements are based on estimates, projections, beliefs and assumptions of management of AGNC at the time of such statements and are not guarantees of future performance. Forward-looking statements involve risks and uncertainties in predicting future results and conditions. Actual results could differ materially from those projected in these forward-looking statements or from our historic performance due to a variety of important factors, including, without limitation, changes in monetary policy and other factors that affect interest rates, MBS spreads to benchmark interest rates, the forward yield curve, or prepayment rates; the availability and terms of financing; changes in the market value of AGNC’s assets; general economic or geopolitical conditions; liquidity and other conditions in the market for Agency securities and other financial markets; and legislative and regulatory changes that could adversely affect the business of AGNC. Certain factors that could cause actual results to differ materially from those contained in the forward-looking statements are included in AGNC’s periodic reports filed with the SEC and available on the SEC’s website at www.sec.gov. AGNC disclaims any obligation to update or revise any forward-looking statements based on the occurrence of future events, the receipt of new information, or otherwise.

We use our website (www.AGNC.com) and AGNC’s LinkedIn and X accounts to distribute information about the Company. Investors should monitor these channels in addition to our press releases, SEC filings, and public conference calls and webcasts, as information posted through them may be deemed material. Stockholders and other interested parties may sign up to receive AGNC’s news, perspectives, and other types of email alerts by clicking the Subscribe link below.